Artificial intelligence (AI) stocks have been in huge demand from investors since last year. The primary catalyst for the AI stock frenzy was OpenAI’s release of its ChatGPT chatbot in late 2022, which showcased the amazing capabilities of generative AI.

This big boost in demand for AI stocks has significantly driven up the prices and valuations of many of them. The high valuations of some AI stocks make them quite vulnerable to major pullbacks or worse. But there are still some relatively little-known stocks of quality and profitable companies involved in AI that have reasonable valuations.

This article highlights one of them: Parsons (NYSE: PSN). To be clear, my favorite AI stock remains Nvidia. But Parsons is worth considering buying by investors who are interested in an AI stock with lower risk and volatility profiles than Nvidia and other AI chip makers.

What does Parsons do?

Parsons, which is based in a Virginia suburb of Washington, D.C., was founded in 1944 and held its initial public offering (IPO) in May 2019 at $27 per share. This turned out to be a tough time to go public, as the company’s business suffered after the COVID-19 pandemic struck in early 2020. But Parsons’ business and stock have rebounded robustly over the last couple of years.

The company describes itself as a “leading disruptive technology provider in the global defense, intelligence, and critical infrastructure markets, with capabilities across cybersecurity, missile defense, space, connected infrastructure, and smart cities.” The range of the company’s capabilities and projects is impressive.

Parsons does work for the U.S. government — including the military and intelligence agencies — and for commercial customers. It also does government work for some U.S. allies. In the first half of 2024, it generated revenue of $3.21 billion — 59% from its federal solutions segment and 41% from its critical infrastructure segment.

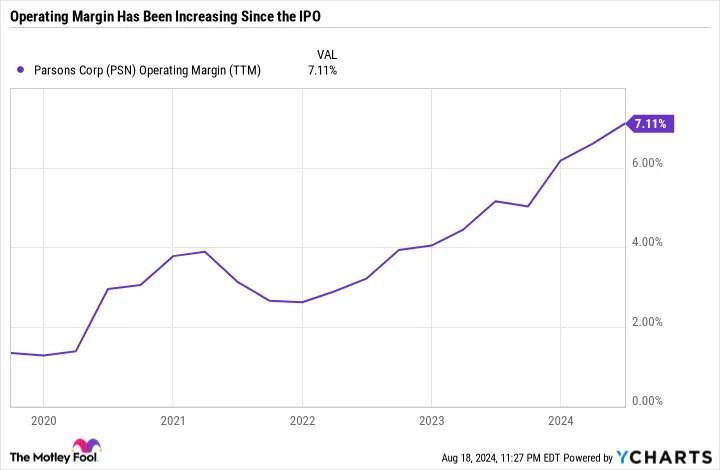

In recent years, Parsons’ management has “transformed the company into a high-value solutions provider that differentiates by leveraging software and cutting-edge technology,” as CEO Carey Smith highlighted in the company’s Q2 earnings release. The “cutting-edge technology” includes AI, which the company is using extensively across its business. This transformation is driving increased profitability, as the following chart shows.

Parsons works with Nvidia, whose graphics processing unit (GPU) chips and related technology are largely powering the AI revolution. Nvidia is one of Parsons’ partners in Parsons X, a general partner network, and in Parsons’ Paladin Lab, a defense-focused “place for our partners and us to experiment, iterate, and invent customer-focused solutions together.”

Parsons’ key numbers

| Company | Market Cap | Forward P/E | Wall Street’s Projected 2024 EPS Growth | Stock Return YTD 2024 | Stock Return Since May 2019 IPO |

|---|---|---|---|---|---|

| Parsons | $10.0 billion* | 29.4 | 31.7% | 50% | 248% |

| S&P 500 | N/A | N/A | N/A | 18.4% | 112% |

Data sources: Yahoo! Finance and YCharts. EPS = earnings per share. YTD= year to date. *A market cap of $10 billion makes a company on the borderline between a mid-cap and large-cap stock. Data as of Aug. 20, 2024.

Parsons stock is having a great 2024. This performance is being driven by the company’s strong recent financial results (not simply the AI mania that’s the exclusive or primary driver of some AI stocks), as we’ll get to in a moment.

Parsons stock is trading at just over 29 times its projected 2024 earnings. This isn’t a cheap valuation, but it’s reasonable for a high-quality company (long-established, profitable, solid cash flows, extremely high 99% institutional ownership) that Wall Street expects to grow earnings per share (EPS) by nearly 32% this year.

Investors should note that Wall Street is projecting that Parsons’ EPS growth will decelerate to 14.4% in 2025. However, the company has a good track record of easily exceeding analyst consensus earnings estimates, so there’s good reason to believe it will continue to do so.

Strong recent financial results

In the second quarter, Parsons’ revenue jumped 23% year over year to a record $1.67 billion, beating the $1.56 billion Wall Street had anticipated. Organic revenue growth was 22%, while acquisitions made within the last year contributed 1% of growth. The quarter was the fifth consecutive quarter with year-over-year organic growth above 20%.

Adjusted net income was $90 million, or $0.84 per share, up 33% year over year and sprinting by Wall Street’s estimate of $0.69 per share. Cash-flow growth was even more impressive. Cash flow from operations was $161 million, or 7 times the year-ago period’s.

Lower-than-average stock price volatility

| Company | 1-Year Beta |

|---|---|

| Parsons | 0.8 |

| Nvidia | 2.4 |

| Advanced Micro Devices (AMD) | 2.2 |

| Microsoft | 1.0 |

| S&P 500 | 1.0 |

Data source: YCharts.

A stock’s beta reflects its price volatility relative to the broader market, or the S&P 500. Parsons stock’s 1-year beta of 0.8 means that its price has been only about 80% as volatile as the overall market over the last year.

AI chip stocks, including Nvidia and AMD, have high betas, reflecting their big price swings over the last year. I included Microsoft as a good example of a big player in AI that’s not a chipmaker. Its stock’s beta is average, relative to the market.

Stock price volatility is not necessarily a bad thing. That said, not all investors are comfortable with stocks that regularly have big price swings. For those folks, Parsons is worth further exploring.

Should you invest $1,000 in Parsons right now?

Before you buy stock in Parsons, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Parsons wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $779,735!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Beth McKenna has positions in Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

This Little-Known Artificial Intelligence (AI) Stock Is Up 50% in 2024. The Company Is an Nvidia Partner With Rising Profitability. was originally published by The Motley Fool